Neobanks

have been able to service Small and Medium Businesses with high efficiency

since they are built on a modern technology stack which is internet-first and

saves on the costly (and questionably – redundant) network of physical

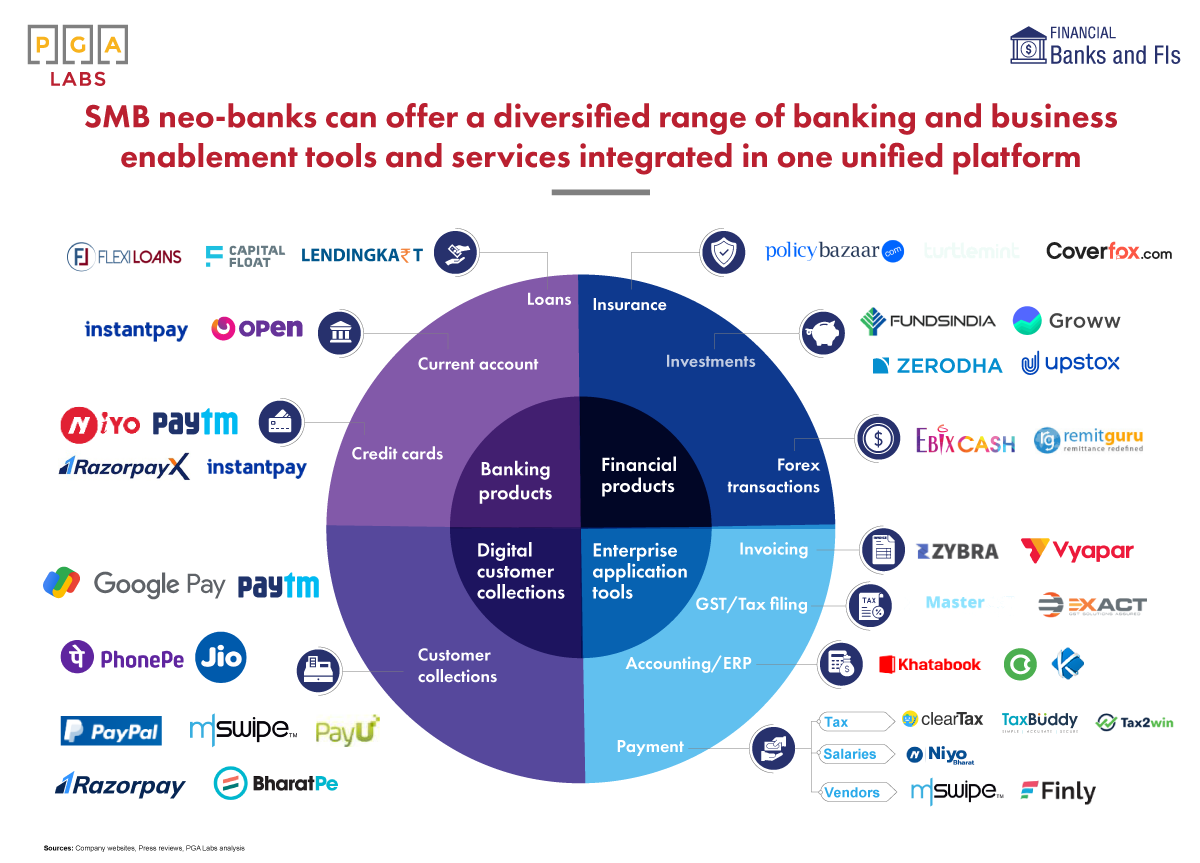

branches. SMB neo-banking is a US$ 6B+ market opportunity, offering diversified

products in each of banking products, financial products, enterprise application

tools and digital customer collections.

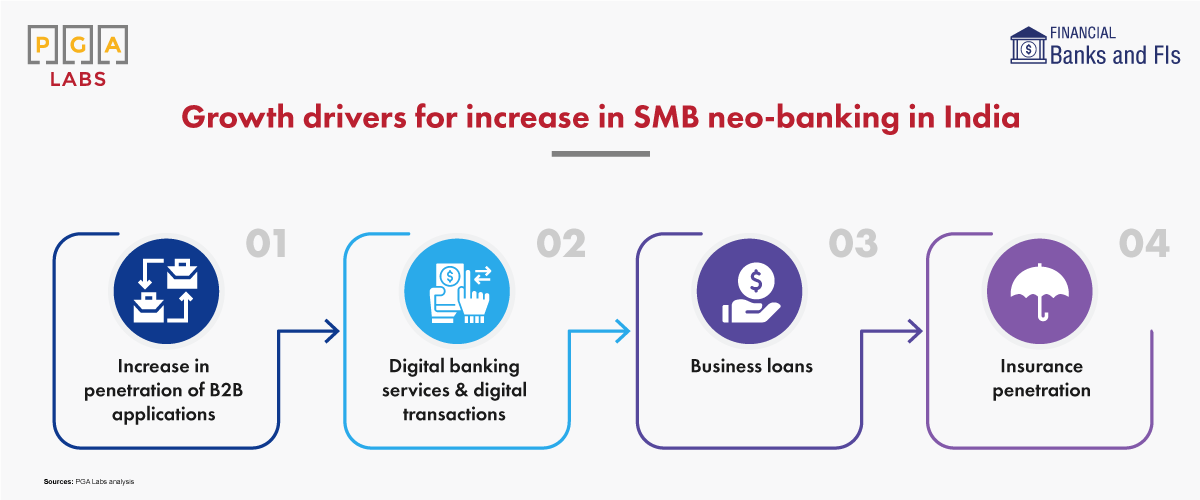

The market is growing on the back of 4 major growth drivers:

- With

the increase in digital penetration, SMBs are adopting technological tools to

streamline their business management like accounting, invoicing, payroll

solutions, and other similar offerings

- Digital transactions are expected to go up from the current 100M per day to 1.5B per day in 2025 leading SMBs accessibility to digital banking services like net banking, wallets, UPI etc.

- Large unmet credit demand that neo-banks can cater (INR 25 Trillion), especially given more than 84%+ avail this from non-formal channels

Attractive SMB customized policies to be launched by IDRAI to increase insurance penetration, currently underpenetrated at ~5%

While Neobanks seem to ‘disrupt’ banking services, traditional banks also have a lot to gain from these partnerships:

- Neo-banks act similar to Direct Selling Agent (DSA) for the traditional banks to onboard new customers, at better CACs. Banks typically spend ~5X to acquire the same customer

- Superior UI/UX design and the tech-stack of the Neobanks provides better experience to the customers, difficult for traditional banks to build and evolve rapidly

- Access to customer data, enabling cross-sell opportunities that are core to full-scale banks, largely untouched by Neobanks

- Access to newer markets, especially regional and interior parts of country where physical presence may not be economical

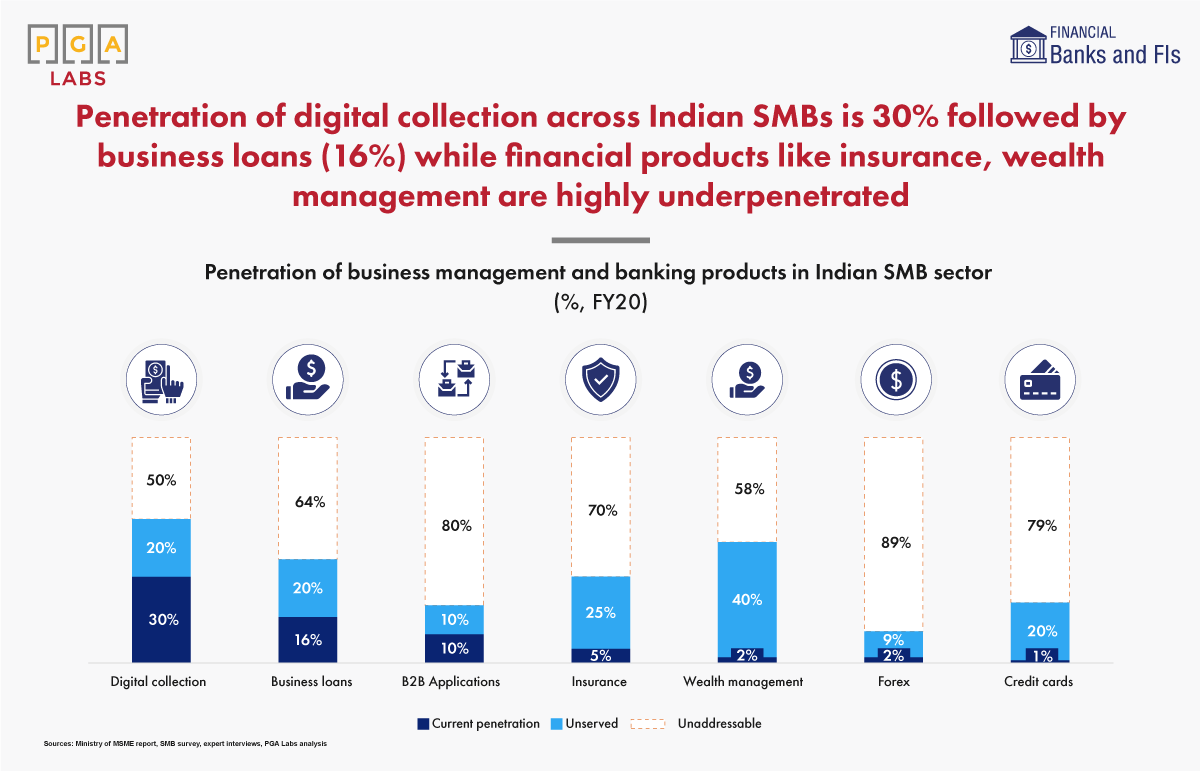

Even

with such strong value propositions, business management and banking products

are unlargely derpenetrated in the Indian SMB market – with immense potential

to unlocked through FinTech.

Authored by (at the time of writing):

Vaibhav Tamrakar, Senior Vice President - PGA Labs